Setting up accrual accounting in Rundoo

What is the purpose of this guide?

To share how you can use Rundoo with the accounting software of your choosing for accrual accounting. This includes:

Getting the data you need to generate important financial statements (e.g., income statement) into your accounting software

Determining the amount of sales tax owed, if applicable. You still pay externally, but you can find the amount in Rundoo.

What are the steps to set up accrual accounting with Rundoo?

To start out, ensure the inventory valuation in your accounting software matches the inventory valuation in Rundoo. If it does, great, you’re all good to go! If it doesn’t, please see Appendix A below on inventory adjustments.

Once your inventory valuations match, there is nothing else that needs to be set up! Instead, Rundoo surfaces the data you need to do your accounting and you can enter that data via journal entries in the accounting software of your choosing — the rest of this article references QuickBooks, but this works with Xero, or any other accounting software! We recommend making these transfers at least once per month, but you can do so on whatever cadence works for you and your business.

What journal entries do I need to create?

There are 2 journal entries that you’ll want to create in your accounting system. We describe below where to get the information currently in Rundoo, and we are working on a report that lists the journal entries exactly as they need to be copied over.

1. Journal entry for Revenue

Why do I do this?

So you can compute Total Income for your income statement and Accounts Receivable for your balance sheet.

What is an example of what this journal entry looks like?

There are different ways to do this journal entry, and the differences mostly concern the level of granularity desired for different accounts. At the minimum, we recommend recording the following for each location: your total bank deposit, credit card fees, returns, accounts receivable, payments on account, non-taxable sales, sales (excluding non-taxable sales), and sales tax payable.

Where do I find the data I need for this journal entry in Rundoo?

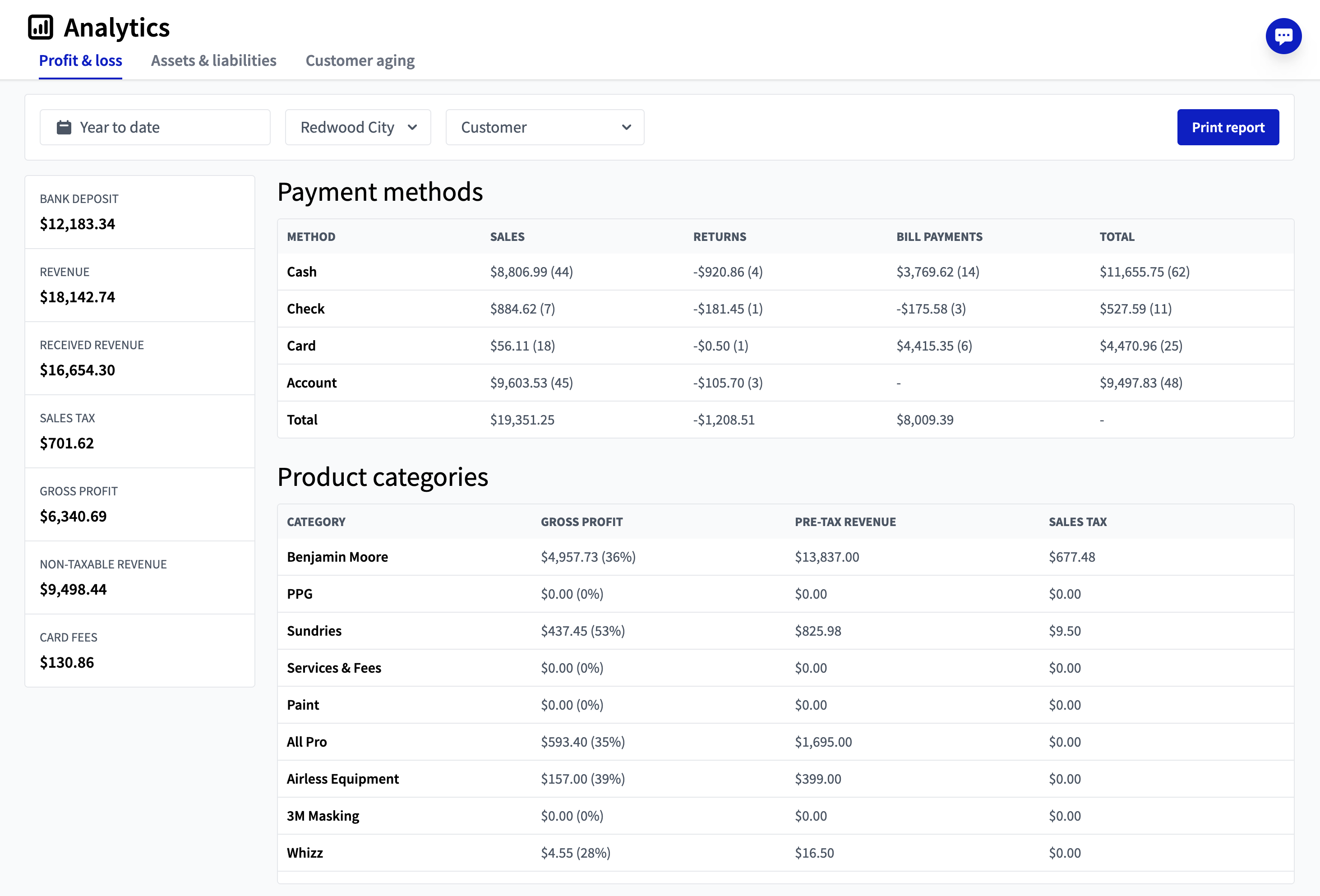

Under Analytics >> Profit & Loss.

If you have multiple locations, filter the data by location, and change the date range to match the relevant accounting period. Then, enter the following:

Debit your bank / cash account: this is the amount deposited in your bank over the period, which includes sales done with cash, check, and card, as well as payments on account. You can break this down however you’d like (or lump it into one sum), but to get these totals from Rundoo you can do the following:

Card deposit: Your card revenue will be automatically deposited in your bank with processing fees already assessed. This deposit will happen on a daily basis, ~24 hours after the close of the prior day. So, the total card deposit for May 1st will come through on May 2nd (Saturday’s and Sunday’s sales are deposited with Monday’s sales on Tuesday). You can check this deposit number ties out in Rundoo by taking the Card Revenue number (in the Total Column and Card Row) and subtracting out “CARD FEES” (in the left hand side column).

Cash deposit: You have to deposit cash into your bank account. You can check your Cash Revenue number in the Total Column and Cash Row.

Check deposit: You have to deposit checks into your bank account. You can check your Check Revenue number in the Total Column and Check Row.

Debit card fees: Fees from card processing. Copy the number from “CARD FEES” in the left side column. Debit this to your card expense account, “Credit card fees.”

Debit returns: The amount you did in returns, across all payment methods. In the “Payment methods” table, take the total value in the Returns Column and debit it to “Returns” (as a non-negative number).

Debit accounts receivable for sales on account: this is the amount to add to A/R at the end of the accounting period. Take the value in the Total Column and Account Row and debit it to “Accounts Receivable”.

Credit accounts receivable for payments on account: this is the amount to subtract from A/R at the end of the accounting period based on bills paid down. In the “Payment methods” table sum, take the total value in the Bill Payments column and credit it to “Accounts Receivable.”

Credit sales: total sales across all payment methods, including sales on account. Importantly, this does not include non-taxable sales and does not includes sales tax (which are reported separately). Take the total value in the Sales column, subtract “NON-TAXABLE REVENUE” and “SALES TAX” from the table to the left and can credit the result to “Sales of Product Income.”

Credit non-taxable revenue: these are sales that tax-exempt, often to a government organization. Copy the number from “NON-TAXABLE REVENUE” field in the left side column and credit to “Non-taxable revenue.”

Credit sales tax payable: this records the sales tax you owe on sales across all payment methods. Copy the number from “SALES TAX” in the left side column and credit it to “Sales tax payable.”

2. Journal entry for Inventory and Cost of Goods Sold (COGS)

Why do I do this?

So you can update COGS for your income statement and Inventory Valuation for your balance sheet

What is an example of what this journal entry looks like?

For each location, you debit (increase) your COGS account for the relevant amount over the period, and credit (decrease) your inventory valuation for the same amount over the period (Note: In the below journal entry example, there are line items for two locations, Menlo Park and Redwood City)

Where do I find the data I need for this journal entry in Rundoo?

To calculate COGS, you are going to subtract the inventory valuation in Rundoo at the end of the period from the inventory valuation in QuickBooks at the end of the same period (if you want to read more about why this produces COGS for the period, please see Appendix A below)

To find your inventory valuation in Rundoo, go to Analytics >> Assets & Liabilities.

If you have multiple locations, I recommend filtering the data by location, so you can report by location in QuickBooks. You can use the QuickBooks “Class” field to specify the location (or just write it in the description as shown in the above QuickBooks Online example).

Filter to the date at the end of the period for your journal entry, (eg, if you are doing a journal entry for the month of March, ending date is March 31st). Copy the number under “Inventory Valuation.”

Subtract this number from the corresponding inventory valuation in QuickBooks — debit the result to COGS and credit the result to inventory asset in a journal entry dated to the last day of the accounting period. Do this for all locations and you’re done with COGS!

What are the next steps?

That’s it! If you have any questions or feedback, feel free to book a time here or shoot me an email at max@getrundoo.com — I’m happy to chat.

Appendix A — inventory adjustments

Complete a physical inventory and make the necessary adjustments in Rundoo (both to quantities and costs) to ensure inventory is accurate

Ensure you have an “Inventory adjustment” account set up as a sub-account within COGS in your chart of accounts

Using Rundoo’s inventory valuation as a source of truth, “true up” your QuickBooks inventory valuation with an adjustment:

If Rundoo has a greater inventory valuation than QuickBooks, debit your “Inventory Asset” account for the difference, and credit your “Inventory Adjustment” account to balance the entry

If Rundoo has a lesser inventory valuation than QuickBooks, credit your “Inventory Asset” account for the difference, and debit your “Inventory Adjustment” account to balance the entry

Check to ensure the inventory valuations are now the same between the two platforms — if they are, you’re all set!

Appendix B — how does this COGS calculation work?

Let’s start by looking at how each inventory valuation is composed:

QuickBooks inventory: Since QuickBooks does not have access to any sales transacted over the accounting period, the ending inventory value only reflects your beginning inventory + purchases over the period (assuming you do your purchasing in QuickBooks)

Rundoo inventory: Since Rundoo sees sales and purchases, the ending inventory value in Rundoo reflects your beginning inventory + purchases - cost of sales

As you can see, the only difference between the two values is the cost of sales. Therefore, if you subtract the Rundoo inventory valuation from the QuickBooks inventory valuation, you will cancel out beginning inventory and purchases over a period and end up with COGS!

Appendix C — other FAQs

How do I log in to Rundoo?

Launch the POS in your browser by loading your domain, select a location from the drop down, click “Sign in using SMS” at the bottom of the screen, type your login code on your keyboard (your initials of first name and last name), check your mobile phone texts for your log-in code and enter it.

When do I transfer data from Rundoo to QuickBooks?

I recommend waiting no longer than the end of each month. Some paint stores do their journal entry once every week or once every two weeks.

What is the role of Stripe Express?

Stripe Express is a mobile app that allows you to see your daily card deposits on the fly. It’s redundant with the reporting you have in Rundoo.

Do I need to change how I enter and pay my bills from my vendors?

For your vendors (e.g., utilities) that didn’t flow through your POS, nothing will change.

For yours vendors that you receive POs from in your POS, things will change. In QuickBooks, you will create and pay these bills like you do with vendors that didn’t flow through your POS:

Create Bill by selecting a vendor and entering the total amount due

Below the total amount due, select the “Expenses” tab, (rather than the “Products” tab) and allocate that total amount to your relevant accounts as line items (generally Purchases and Shipping & Freight)

Once the inventory is received, credit your Accounts Payable (if the original ordered inventory amount was not received, adjust the bill as needed).

Once you pay your bills, debit your Accounts Payable and credit cash (this may happen automatically if you pay in QuickBooks)

How do I determine how much the business owes in taxes to the municipality, county, and state?

Pull total sales tax $ from Rundoo for a period (see “SALES TAX”). The process on paying sales tax varies by state:

In some states (e.g., California), you pay one lump sum of tax to the state. This lump sum will be the “SALES TAX” in Rundoo’s Profit & Loss page. The state then disperses the tax you pay to your municipality, county, and state.

If other states, (e.g., Colorado), you have to determine and pay the tax amounts owed to each of your municipality, county, and state. You can find these amounts by dividing each individual tax rate (e.g., the municipal tax rate) by the total sales tax rate. For example, if your total sales tax in Rundoo is $1,000, your total sales tax rate (municipality, county, and state combined) is 10%, and your municipal portion of that 10% tax rate is 2%, then you owe $200 in municipal taxes ($1000 x 2% / 10% = $200) with the rest going to county and state.

What data lives solely in QuickBooks?

Income statement, balance sheet, and cash flow statement

Bills from your vendors / utilities.

Accounts Payable & payroll

This is not financial advice. Please consult your trusted tax professional before making these types of decisions.