Accounting 101: Assets = Liabilities + Equity 🧮

Plus omni-search, custom sales tax rates, and order fees & discounts

Last week, we wrote about our new accounting suite. A big thank you to those that reached out to start the transition! The process is shaping up to be:

Transfer chart of accounts and balances: Y’all send us an income statement and balance sheet, and we set up your chart of accounts with opening balances.

Define categorization process: We review together your income and expenses to ensure you have a good process of logging them in Rundoo.

If you have not reached out but are interested in learning more, please book time on my calendar.

Today will be a tad different from normal!

First, we’ll cover three product updates similar to any other Rundoo Primer. However, we’ll then do a very general accounting overview, completely unrelated to Rundoo! Why? We’ve found a number of clients feel very uncertain about their understanding of accounting. We hope that in the process of moving things over to Rundoo, you can hone this understanding while cleaning up your books.

Let’s do it.

Three quick product updates

1) Omni-Search

Let’s say you are looking for the last time you tinted an Ultra Spec product in Chantilly Lace.

Before: You went Sales > Sold, and searched across ANY field. Because it would only match to one field, you had to filter to “Chantilly Lace” and search for Ultra Spec.

Now: You can go to sales > Sold and can search across ALL fields. You can just type “ultra spec chantilly” and it will show up.

2) Customer Custom Tax Rates

Let’s say you have a customer that isn’t taxed at the default sales tax rate at your location (because, for example, they are a farmer in California).

Before: Every time you sold something to this customer, you had to adjust the tax rate.

Now: You can assign the customer a custom sales tax rate that will automatically be applied to every sale going forward.

If you’re interested, we wrote more about sales tax in Rundoo a couple months ago.

3) Order Fees & Discounts

Let’s say a vendor charges you some fee or discount that is not related to a specific product, like freight, split case surcharges, or early payment discounts.

Before: Every time you made an order with one of these fees, you had to either ignore the fees (which meant your purchase orders didn’t match your invoices) or add them as products (which meant they affected your inventory).

Now: You can add a fee or discount mapped to any cost of goods sold account. This means that your invoice matches your order and your inventory stays accurate.

Accounting 101

Ok, let’s jump into a general accounting overview! As always, we are not tax experts, this is not tax advice, and you should consult your accountant or tax adviser with any questions.

1) The Accounting Equation: Assets = Liabilities + Equity

Accounting starts with a list of asset, liability, and equity accounts (collectively, your chart of accounts) that reflect what the business owns, owes, and has earned:

Asset = business owns

Example accounts: Cash, Accounts Receivable, Inventory

Liability = business owes

Example accounts: Accounts Payable, Sales Tax Payable, Payroll Taxes Payable

Equity = business earned

Example accounts: Stock, Retained Earnings, Sales Revenue, Interest Revenue, Cost of Goods Sold, Credit Card Expense, Rent Expense, Salary Expense

The accounting equation simply says that the sum of all asset account balances must, at all times, equal the sum of all liability and equity account balances. Why? Because equity represents what would be left over all assets were sold and all liabilities were paid (A - L = E).

The balance sheet is simply the balance of all accounts at a given time. It’s called the balance sheet because the account balances on the two sides (assets on one side, liabilities and equity on the other) must sum to the same number. That is, they are balanced.

What about income and expenses? They don’t show up on the balance sheet. Instead, the difference between all income and expenses shows up as an equity account called Retained Earnings. In this sense, income and expense accounts are like equity accounts, which is why I included them under “Equity” above.

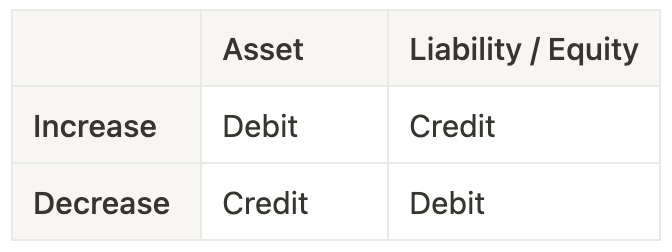

2) Debits (increase Assets) = Credits (increase Liabilities or Equity)

Every transaction that occurs in a business impacts two or more accounts. These impacts take the form of either debits or credits.

Debits are increases in asset accounts and decreases in liability or equity accounts.

Credits are increases in liability or equity accounts and decreases in asset accounts.

Please enjoy the world’s simplest table:

What about income and expenses? Income follows the same convention as equity: credits are increases, and debits are decreases. Expenses are the reverse.

Now, remember our accounting equation? Assets = Liabilities + Equity. Because of this, the net change in assets must also equal the net change in liabilities and equity. So debits (which represent half of this net change) must also equal credits (which represent the other).

3) Examples: Journal entries and the resulting balance sheet

Before we look at some examples, how is all of this activity recorded?

Journal entries debit and credit the accounts to increase and decrease their balances. Journal entries are called double-entry because each journal entry MUST have debits and credits that sum to equal one another.

Journal entries are captured in a general ledger, which is essentially a giant spreadsheet detailing all transactions. The general ledger contains (1) the timestamp of each transaction, (2) the accounts impacted, and (3) whether those accounts were debited or credited.

Now, for the examples, all of which live in this spreadsheet. Note that the following transactions are cumulative, i.e. each step builds on the previous.

Owner investment: We debit our cash account (an increase in our assets) and credit our stock account (an increase in our equity).

Receive inventory: We debit inventory and credit accounts payable.

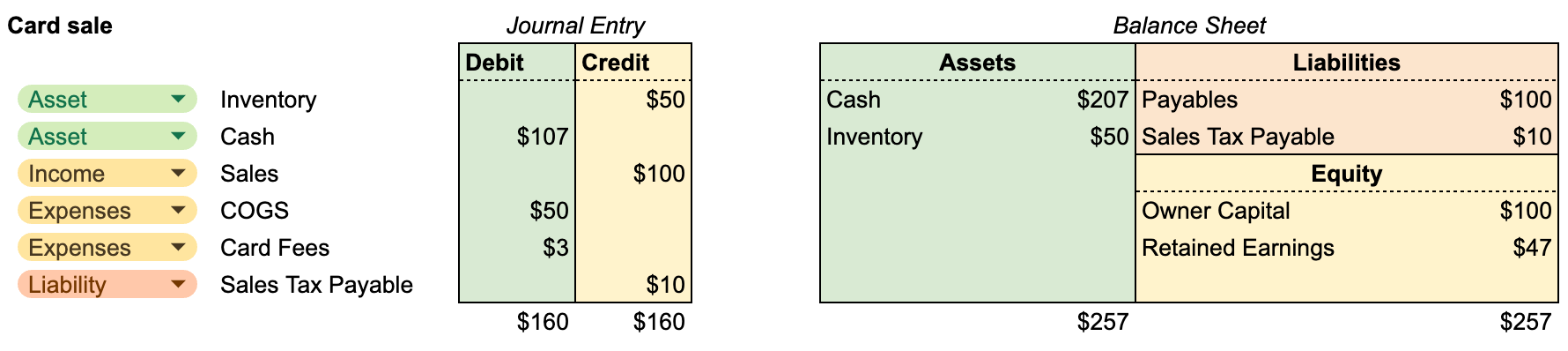

Card sale: A big one! We credit inventory because products left the store, debit cash the sale total net of card fees that hits the bank, credit sales the pre-tax total because tax isn’t revenue, debit cost of goods sold (COGS) the cost of the inventory, debit card fees any fees collected, and credit sales tax payable the sales tax. Phew! 😤 Remember that debits and credits to income and expense accounts are netted and hit the balance sheet as “Retained Earnings.”

Charge sale: This is the exact same as the above example except (1) instead of debiting the total to cash, we debit accounts receivable to be paid later, and (2) there are no card fees.

Account payment on card: We debit our cash and credit our accounts receivable, with some card fee expenses hitting retained earnings.

Interest: Interest is revenue! So we credit the interest income account and debit receivables.

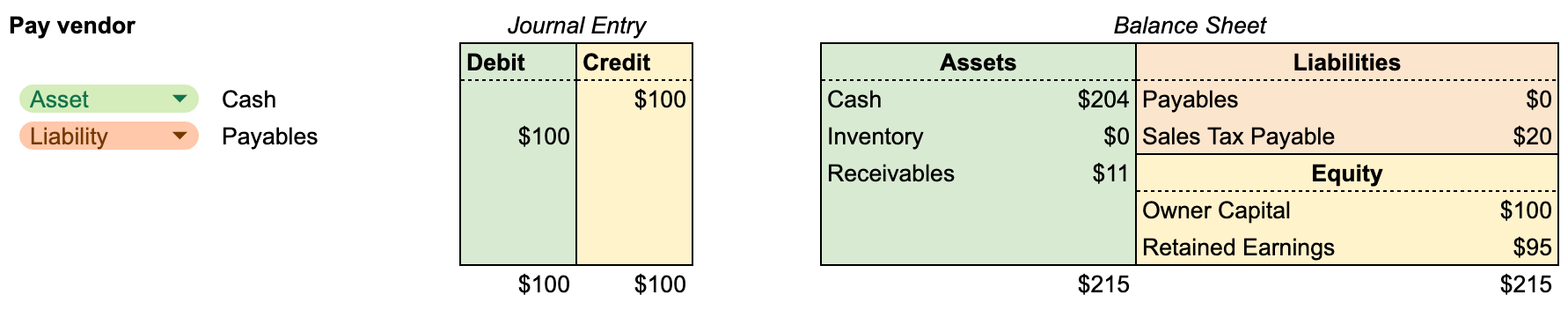

Pay vendor: Credit the cash used to pay, and debit the payables down.

What next?

If you made it this far, you’re a champ—thanks for following along. While knowing this is undoubtedly helpful in running a business, good bookkeeping software tracks all of this under the hood for you so that you can focus on other things. That is the goal!

As always, reach out if you have any questions.

👋